In January 2022, we released our first-ever annual predictions covering the work of Main Streets and anticipated impacts on small businesses that make up the fabric of our downtowns and neighborhood commercial districts. Making predictions is always a risky proposition but is a valuable pursuit to get a better idea of what to keep an eye out for in the coming year. Perhaps an even more risky proposition is to take a reflective look back to see what was on target, what was a mixed bag, and what we got wrong. So, before we dive into what we expect to see in 2023, let’s take a look at a few of last year’s predictions and see how they played out.

GOT IT RIGHT: Main Street Workforce Constraints Remain, Resulting in Accelerated Technology Integration and Further Business Model Shifts

Unemployment remained low throughout 2022, with recent layoffs primarily impacting the technology sector. Stories abounded throughout the year of small businesses continuing to make shifts or integrating technology. One of these stories landed on the front page of the September 26th edition of the Wall Street Journal that covered a Milledgeville, Georgia, plumbing company from our entrepreneurial ecosystem work with partner Georgia Power and Georgia Main Street.

MIXED BAG: Certain Retail Sectors Will Continue to Grow While Others Level Off

“Looking ahead at opportunities for continued growth in our downtowns and commercial corridors,we should anticipate that retail spending around health and fitness (e.g., sporting goods up 29.9 percent), home improvement, furnishings (e.g., furniture up 28.2 percent) décor and gardening will continue to grow in 2022.”

But for our Main Streets, whether small downtowns or neighborhood commercial districts, the office sector is more centered on the office-service sector in which interaction with clients is more prevalent—think your local real estate or insurance office. As such, while some shifting occurred, it was far more limited and less disruptive than thought when we made the prediction in early 2022.

So, while no forecast is always perfect, taking the time to better understand trends and how they might impact the work of place management and small business is still a valuable planning activity that can help to inform the coming year. As such, I spent some time looking ahead to 2023 and landed on five key areas to consider, investigate, and discuss in the coming year.

For decades, the U.S. ecosystem hubs were concentrated along the coasts (think California’s Silicon Valley and Boston’s Route 128 Technology Corridor). Due to technology business relocations and consolidations in finance, places like Austin, D.C., Chicago, Charlotte, and Atlanta, have witnessed an acceleration of greater talent concentrations over time.

One key to success in these regions has been the concentration of human capital combined with the density of place that creates both intentional and accidental collisions that in turn form new ideas, access to capital, and networks that are the hallmark of successful small business support systems. However, the global pandemic has shifted both. For example, the rise of remote work, which has primarily been in the technology office sector, provided opportunities for human capital to decouple from these areas, diffusing this workforce to often suburban and rural locations. And now, these tech and financial centers are faced with what Professor Scott Galloway has coined the “Patagonia Vest Recession.” More on the long-term prognosis for Big City downtowns can be found in this recent analysis piece from Architecture Magazine.

As I indicated earlier, the office sector was largely unimpacted in most small and mid-sized cities. The heavy migration of remote work talent and recently-retired individuals to these areas provides the ingredients necessary to greatly enhance and stimulate a series of micro ecosystem hubs around Main Streets. They will likely never make the headlines or even be “named,” but nevertheless will have profound impacts on these communities’ overall economic growth and resiliency.

I spent time last year in Jasper, Georgia, where new businesses were popping up all over downtown and an entrepreneurial vibe was evident in meetings with both newcomers and existing residents who saw newfound energy in the community’s economic prospects. According to the Internal Revenue Service’s migration data from 2019 to 2020, there were 1,502 tax filings representing 2,972 new residents in Pickens County (Jasper, Ga.). The 2020 population for the county was 34,032 with newcomers representing a nearly 9 percent increase and an income injection into the economy of over $131 million!

For many years we have focused on place-based assets. As Main Street organizations we should begin to better understand our existing and new human capital assets and leverage place-based and organizational assets that create these accidental collisions—from obvious third places like cafes, breweries, and libraries, but also through our own task forces and other volunteer activities that enable us to capture talent. That is what will begin to drive and grow our own ecosystems. Think human capital asset mapping!

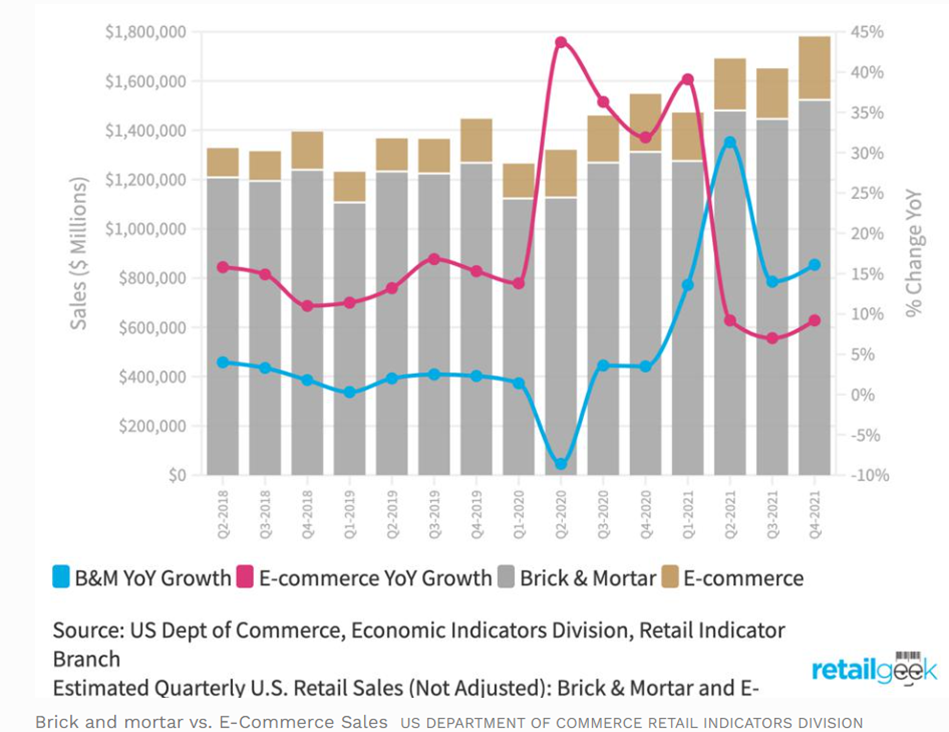

Yes, I know many of you may be thinking “when did that happen?!?” Certainly, in early 2020 the rate of e-commerce sales growth was off the charts—in fact, during an 8-week period in March and April 2020, e-commerce growth exceeded the equivalent of what occurred in the previous decade. But what we have also witnessed during the global pandemic is an unexpected awakening, with consumers realizing what they missed when it was gone: the experience of going into a store, interacting with other humans, seeing family or neighbors, and just being able to use their senses as part of shopping. We had missed this essential form of leisure. In fact, the tide had already begun to turn in 2021. In evaluating the following graphic with data from the U.S. Department of Commerce, bricks-and-mortar sales growth began to surpass e-commerce sales growth during the first quarter of 2021, and throughout the year kept a consistent 6-7 percent growth advantage.

As we look ahead into 2023, a couple of things are already shedding light on this prediction coming to realization. First, the sizable stock price declines and recent announced layoffs from Amazon. While 20,000 sounds like a lot, given their size it’s still fairly small. However, this certainly marks a shift from the hiring frenzy of 2019/2020. And, the fact that much of the anticipated layoffs are occurring in distribution further suggests headwinds for online ordering.

Secondly, several exclusively online brands announced that they would be moving into the bricks-and-mortar space. One could argue this started with Apple. And now we see what was seemingly a purely transactional online experience transform into a closer alignment between the brand and the lifestyle feeling that a company attempts to evoke through an instore purchase. Some brands recently making this switch include Warby Parker, Bonobos, Allbirds, and Amazon (through various iterations including partnerships with Kohl’s and Starbucks).

Hmm, perhaps they realize something we Main Streeters always knew: people like human interaction and the experience of being around others, even if that means just sitting in a coffee house with a $6 latte by themselves.

During the pandemic there were a number of particular retail sectors that experienced sizable growth. For example, retail bike sales grew by 54 percent from April 2019 compared to April 2021. Sales and interest in garden sheds grew by 400 percent. And in April 2021—powered by consumers having extra-large covid relief tax refunds—furniture sales were up 181 percent over the previous months. But that was then, and as we saw in 2022, overall retail sales began to reach some norm-setting more consistent with 2019 than 2021. Inflation headwinds are part of the equation, but the fact is that 2021 was such an incredible spending year that in 2022, many consumers already had a lot of what they could not get in 2020. As such we would anticipate consumers will now direct more of their spending to servicing those past purchases and more leisure experiences. So, what does that look like for Main Streets? Time to work with our retailers to add more service elements!

For bike stores: more servicing elements, groups rides, and perhaps joint service promotions with travel agents for bike excursions. While bike sales are down, bike riding as a form of recreation remains very strong—just ask our friends over at Rails-to-Trails.

For clothing, shoe, and other fashion retailers: repair services. Yes, even Tommy Hilfiger and Hugo Boss are launching repair services as part of a movement toward more eco-friendly “repair, reuse, and recycle” shifts in consumers. It’s one way to keep the consumer engaged in your store when inflation threatens a pullback in new sales.

For restaurants: more cooking classes and online video tips. Consumer dining remains strong, but eventually that will start to pull back with economic shifts and diners realizing all the home improvements they made during the pandemic could be more fully utilized. This is another way to keep customers engaged and coming back.

Much of the news cycle over the past year has reflected on our younger generations through the lens of workforce participation. In fact, Gen Z will make up 30 percent of the workforce by 2030. But for Main Street, 2023 will mark a highly visible shift in asset ownership along our neighborhood and downtown commercial districts. The context for this prediction simply comes from observations throughout visits to 50 plus communities in 2022 in which whether it was focus groups of entrepreneurs or district tours, there was an obvious youth movement.

The Grant Building Project in Downtown Bath, Maine; Jon Stein, owner of Fogtown Brewing Company.

And in Ellsworth, Maine, I met up with Jon Stein, owner of Fogtown Brewing Company and an example of what we had historically thought of our long-standing business owners…those that served on committees and had a deep level of community engagement. I visited Jon on election day. That evening he found out he won election to Town Council.

These are not isolated examples as my travels have demonstrated a highly visible shift is afoot. Despite the often doom and gloom of the passing torch from one generation to the next, our Main Street’s are in terrific hands and the future is bright.

For years, names like Jamie Diamond, Jeff Bezos, and Elon Musk have dominated the news cycle and even entertainment pages. Some might refer to this as corporate idolatry. In 2023, we believe there is a real opportunity to really showcase and highlight the importance of Main Streets and the small business owners as essential players who make of our neighborhoods and downtowns as critical to one’s quality of place and to what truly brings value to the consumer experience. With the rise of the “covidprenuer,” these past two years have witnessed amazing growth in individuals endeavoring to reach their dreams of business ownership. Many of those individuals chose to launch along our Main Streets for the very reason that they wanted to give back to their community and be a part of something bigger than just their business. This motivation is often missing in corporate America and consumers took notice during the pandemic when businesses were shut down. Join us in the coming months as we begin to push this storyline as part of Main Street’s brand and identity.

In closing, I’m a big believer that innovation occurs at the crossroads of people’s different backgrounds and experiences. While these are just some of my thoughts based on visiting with many of you and your communities throughout the year, pleasereach out and share your own observations. We will continue to monitor these trends and predictions for 2023 and look to incorporate our findings and your experiences into evolving and adaptable planning tools for your Main Street program's continued resiliency.

Community Heart & Soul, a Main Street America Allied Member, is this quarter's Main Spotlight advertiser. For more information about what they do to support Main Street organizations, click here.

The Backing Small Businesses grant program, supported by American Express, is now accepting applications for a round of Disaster Recovery grants. Grant funds will support locally significant and economically vulnerable small businesses that have been impacted by the California Wildfires and other FEMA-declared disasters on or after January 1, 2024. Businesses can apply for one of 100 available $10,000 grants to support their recovery efforts.

Join host Matt Wagner for his conversation on the current economic challenges facing small businesses and the strategies and innovative pivots that can help better navigate these turbulent headwinds.

We’re excited to announce a new series on Main Street America’s online store, Shop Main Street, highlighting the stories behind the amazing brands, makers, and producers along our Main Streets.

On this week's episode, host Matt Wagner visits San Germán, Puerto Rico, for a discussion with Roberto Melendez, owner of local restaurant, Pórticos 1606.

Are you looking for ways to support small businesses in your community? Shopping locally has many benefits, from creating stronger communities to building sustainable economies. Learn how you can support small business owners in your area.

In this episode, host Matt Wagner sits down with Dottie Lange and Dottie McQuade of The Monogram Shoppe in Woodbury, New Jersey to discuss the process and considerations that come with selling a small business.

The 25 small businesses receiving enhancement grants represent 25 states across the country. Earlier this year, each of these recipients also received an additional $10,000 as part of a 500-member cohort.

In this episode, recorded in front of a live audience at the Maine Downtown Conference in November 2024 in Biddeford, Maine, host Matt Wagner explores the world of crowdfunding as a financing alternative for small businesses.

In this episode, Matt and James explore the unique journey of starting a business during the pandemic, the challenges of running a small-town café, and the importance of community connection.

In this episode, host Matt Wagner sits down with husband-and-wife duo, Phoebe and Jonathan Carpenter Eells, co-owners of elSage Designs in Mount Vernon, Washington.

Join host Matt Wagner for his conversation with Patrick Jackowski and Matt Horne, the duo behind Firehouse Coffee 1881, a thriving coffee shop housed in a firehouse in historic Fort Monroe, a decommissioned military compound located in Hampton, Virginia.

In this episode, Matt reveals the data-driven trends that will define the 2024 holiday shopping season—and shows you exactly how to leverage them for your small business.

As we approach this milestone celebration, we've compiled 15 creative ways for Main Street and downtown leaders to make this year's Small Business Saturday truly special.

Calling all small business owners: tell us about the wins you've had in 2024, the challenges you face, and the types of support from the Main Street America network that would help you most. Take our latest survey today!

Join host Matt Wagner as he welcomes Kaycee McCoy, co-owner and creative lead at Pawsnickety Pets in Norfolks, Virginia. Kaycee and her best friend, Shizuka Benton, launched the all-natural and organic pet supply business in Norfolk at the start of the pandemic, but have used their combined talents to keep the business growing and thriving over the last four years.

In this episode of Main Street Business Insights, Matt interviews Patrice Hull, the owner of Stuff We Wanna Say Custom T-Shirts and Apparel and c2bn / Created to be Noticed, based in Atlanta, Georgia.

In this episode of Main Street Business Insights, Matt sat down with Mindy Bergstrom, owner of Cooks Emporium, Nook & Nest, Z.W. Mercantile, and The Recipe, all located in downtown Ames, Iowa.

Our Research team shares the results of the Spring 2024 Small Business Survey, with insights related to small scale manufacturing in Main Street districts, opportunities to best support entrepreneurs, and more.

This specialized learning experience, sponsored by U.S. Bank, combines interactive classroom sessions and a hands-on course project to equip local leaders with insights, strategies, and a a distribution-ready small business guide to foster entrepreneurship, support small business owners, and retain local businesses. Registration closes on Friday, August 30.

In this episode of Main Street Business Insights, Matt sat down with Kristin Smith, owner and founder of The Wrigley Appalachian Eatery in Corbin, Kentucky.

In this episode of Main Street Business Insights, Matt talks with Joshua and Jared Ravenscraft, co-founders of New Frontier, a sustainable apparel brand in Morehead, Kentucky.

Shop crawls are a great way to introduce people to your small businesses. Fredericksburg Main Street loves to host shop crawls, and this spring, they tried a new model: the flower crawl.

If the economic vitality of your downtown is on your mind, Main Street America Institute’s Supporting Small Businesses on Main Street course for you! This specialized learning experience, sponsored by U.S. Bank, will give you new insights, tools, and strategies to foster entrepreneurship, support small business owners, and retain local businesses. Registration closes on Friday, August 30.

In this episode of Main Street Business Insights, Matt chats with Ross Chanowski, owner and founder of NuMarket. NuMarket is a leader in crowdfunding solutions for small businesses with a focus on food services.

In this episode of Main Street Business Insights, Matt talks with Ebenezer Akakpo, a designer and jeweler who owns Akakpo Design Group and Maine Culture in Westbrook, Maine.

American Express and Main Street America announced the 500 small business owners who have been awarded $10,000 through the Backing Small Businesses grant program.

In this conversation, Matt explores the story of Elements: Books Coffee Beer, nestled in the heart of Biddeford, Maine, with co-owners Katie Pinard and Michael Macomber.

We are asking small business owners across the country to share their perspectives on the opportunities and challenges they're facing as summer approaches.

In this special episode of Main Street Business Insights, recorded in front of a live audience during the Main Street Now Conference, Matt sat down with Alycia Levels-Moore, owner and founder of ASL Creative Firm and POLARIS, an event and co-working hub, based in Birmingham, Alabama.

Urban Impact Inc., harnesses strategic investments and collaborative efforts to foster a vibrant and sustainable future, from visionary adaptive reuse ventures to transformative development grants for small businesses and property owners in Birmingham, Alabama's historic 4th Avenue Black Business District.

In the last episode of season two of Main Street Business Insights, tune in as host Matt Wagner breaks down how to understand and synthesize local market data.

Sterling Main Street launched a brick and mortar retail incubator spaces. Executive Director Janna Groharing shares lessons they learned about organization, fundraising, and outreach.

In this episode of Main Street Business Insights, Matt sits down with Glen Ellis, owner of Sycamore Education, Dominion Catalyst Services, and Milady Coffeehouse in Fremont, Nebraska.

In this episode of Main Street Business Insights, Matt sits down with Jaime Courtney, President of Shoalwater Seafood, Derek King, Oyster Farm Director of Shoalwater Seafood, and Shane Thomas, Tribal Council Vice Chair of the Shoalwater Bay Indian Tribe.

Sarah Cole, owner of Abadir’s in Greensboro, Ala., was a 2023 Backing Small Businesses grantee. Abadir’s is a pop-up eatery specializing in seasonal and wholesome baked goods influenced by Egyptian traditions and flavors combined with inspiration from true Southern cuisine.

In this episode of the Main Street Business Insights podcast, Matt sits down with Casey Woods, Executive Director of Emporia Main Street in Emporia, Kansas.

In this episode of Main Street Business Insights, Matt sits down with Nicole Fleetwood and McKinzie Hodges, co-owners of Scratch Made Bakery in Amarillo, Texas.

Tylisya Gober, owner of Barbie Behavior Boutique in Oak Park, Mich., was a 2023 Backing Small Businesses grantee. Barbie Behavior is a women’s clothing boutique specializing in celebrity-inspired attire.

Tiffany Fixter, owner of Brewability in Englewood, Colorado, was a 2023 Backing Small Businesses grantee. Brewability is an inclusive brewery and pizzeria that employs adults with disabilities to brew craft beer.

We’re excited to announce that Main Street America will continue to offer virtual and on-demand small business training in 2024 through an evolved program, the Small Biz Digital Trainers program.

In this episode of Main Street Business Insights, Matt sits down with Jennifer Jones, co-owner of Good Times Coal Fired Pizza and Pub in Big Stone Gap, Virginia.

In this episode of Main Street Business Insights, Matt sits down with Tiffany Fixter, owner of Brewability, an inclusive craft brewery and pizzeria that employs adults with disabilities based in Englewood,

In this episode of Main Street Business Insights, Matt sits down with Bobby Boone, founder and Chief Strategist of &Access. Based in New Orleans, La., &Access creates data-driven and design-centric retail real estate solutions for historically excluded entrepreneurs and under-invested neighborhoods.

Tasha Sams, Manager of Education Programs, shares highlights of phase one of the Equitable Entrepreneurial Ecosystems (E3) in Rural Main Streets Program and the biggest takeaways from the workshop experiences.

In this video, learn more about the Williams’ family story, how the business is helping to revive downtown Helena, and the impact they’re having on a national level.

In this episode of Main Street Business Insights, Matt sits down with Derrick Braziel, owner of Pata Roja Taqueria and co-founder of MORTAR, in Cincinnati, Ohio.

Small Business Saturday is an important opportunity to show your support for local businesses. We asked business owners across the network what your support means to them.

Matt sits down with Jamie and Jerry Baker, co-owners and founders of Trendy Teachers, a teaching boutique and educational toy store located in downtown Rome, Georgia.

Middlesboro Main Street in Middlesboro, Ky., Puerto Rican Cultural Center in Chicago, Ill., and Sugar Creek Business Association in Charlotte, N.C., have each been awarded $100,000 through The Hartford Small Business Accelerator Grant Program in partnership with Main Street America.

Matt sat down with Anette Soto Landeros, co-owner of Casa Azul Coffee and President and CEO of the Fort Worth Hispanic Chamber of Commerce in Fort Worth, Texas.

Matt Wagner sat down with Danny Reynolds, president and owner of Stephenson's, an independently owned high-end fashion retailer in downtown Elkhart, Indiana.

Matt Wagner sat down with The Barbershop Conversation podcast team, co-hosts Kenneth Bentley and Davion Hampton along with executive producer Emory Green Jr., in Goldsboro, Florida.

This three-week live, online course will prepare local leaders to more effectively work with small business owners in their districts and create an environment that is supportive of entrepreneurship.

Meet the 2023 recipients for the Backing Small Businesses grant program, presented by American Express, to provide financial support to small business owners to address critical needs and make a positive impact in their local communities.

In partnership with Grow with Google, our digital coaches will work with businesses in their home states, with a focus on those that operate in small towns and rural communities.

Check out a deep dive into the results of our Spring 2023 Small Business Survey, plus insights to help inform the work of local leaders supporting entrepreneurs on Main Street.

Matt Wagner wrote an article for the OECD blog on how can small business owners can combine digital tools with the power of place to find sustainable success.

Inspired by a session at the 2022 Main Street Now Conference, Main Street Ottumwa has launched the Business Builder Academy, an entrepreneurship course to help aspiring business owners start their ventures.

Whether you are a seasoned American Express Small Business Saturday Neighborhood Champion or an entrepreneur joining this national movement for the first time, we’ve gathered a roundup of resources to support your “shop local” marketing efforts.

We spoke to three women who were awarded Inclusive Backing grants to learn more about their passions, their businesses, and their advice for other women.

From social media scavenger hunts to downtown passports, the Main Street network has used countless innovative ways to encourage their communities to Shop Small®—and had plenty of fun doing it.

#EquityRising, Old Algiers Main Street Corporation's new job training program, seeks to combat rising cost of living by helping residents train for careers that will allow them to stay in their neighborhood.

We spoke to three Black business owners who were awarded Backing Small Businesses grants from Main Street America and American Express to better understand their challenges, successes, and the kinds of support that have helped them the most.

Main Street Skowhegan opened their new Skowhegan Center for Entrepreneurship, a downtown space for co-working, meeting, entrepreneurial support, trainings, and education.

Main Street Charles City organizes their annual 'WonderFall' event, a business decorating contest designed to have some fun with the autumnal season as well as provide a reminder of the importance of curb appeal in attracting the public’s attention.

Leverage NC, a partnership between North Carolina Main Street and the North Carolina League of Municipalities, hosted a four-part webinar series titled Better Community Planning & Economic Development led by Ed McMahon, Chair Emeritus of Main Street America and a leading national authority on land use policy and economic development.

Main Street Arkansas has brewed a new engaging way for tourists and residents alike to explore local Arkansas commercial districts: the Main Street Arkansas Coffee Trail.

We spoke with two Black entrepreneurs in UrbanMain commercial districts: L. May Creations in the Austin neighborhood of Chicago and The Four Way in south Memphis, Tennessee.

We heard from organizations across the nation about the incredible impact their markets have had on community engagement, entrepreneur and small business support, and keeping their district vibrant.

The global pandemic gave us all a glimpse of a further dispersed future – a time when you don’t sit in a classroom at school, watch movies in a theater, or even go to the grocery store. Where do Main Streets fit in that model?

This May marked the 100th anniversary of the Tulsa Race Massacre in the Greenwood neighborhood of Tulsa, Oklahoma. We explored the impact and legacy of this tragic event.

BDOs are place-based organizations that help small businesses and entrepreneurs to flourish. They have been on the frontline of support for the country’s hardest-hit entrepreneurs throughout the pandemic and have been working to enable thriving commercial corridors throughout the crisis.

Matthew Wagner, Ph.D., Chief Program Officer at Main Street America, was featured on Breaking Down Barriers: a podcast from Startup Space highlighting stories of community leaders who break down barriers to entry for underserved and unrepresented entrepreneurs.

We heard from 289 business owners in 35 states plus the District of Columbia in our new text message-based survey of small business owners across the network.

The Batavia Boardwalk Shops are freestanding, purpose-built structures acting as seasonal pop-up locations for entrepreneurs, offered in tandem with a business incubator program.

For Black History Month, we want to recognize and celebrate the Black business owners and entrepreneurs who have overcome challenges and obstacles in launching and running their own businesses, thanks to resilience, creativity, and hard work.

As a vital place factor within an entrepreneurship ecosystem, pop-up programs allow for emerging businesses to test their product, gain consumer feedback, and promote their brand at an extremely low cost. In essence, allowing for a ‘fail-fast’ product development cycle.

In early December, as the COVID-19 crisis intersected with a peak moment in the holiday shopping season, we surveyed small business owners and Main Street programs to learn more about how they were managing.

New research by Main Street America suggests greater returns on our missions and resources can be had by transitioning to more deliberate economic vitality work centered on cultivating new business development from within our own communities and neighborhoods.

Fredericksburg Virginia Main Street (FVMS) is taking storefront activation to a new level with their new initiative, the Scan & Love Project, which tells the stories of business owners through personal and engaging videos.

Read the results of our survey aimed at understanding how business owners are managing the recovery from COVID-19 and responding to recent protests and social unrest related to police violence against Black Americans.

Our research team dug into some of the data about the state of Black-owned businesses on Main Street, the structural challenges they face, and how Main Streets can support them.

Detailed findings from our follow-up survey on the impacts of COVID-19 on small businesses to better understand the continued challenges businesses face as the crisis evolves.

Small Business Saturday® is more than a day to shop. It’s a nationwide movement that shines a spotlight on the importance of supporting small businesses in communities across America.

The Berkley Downtown Development Authority (DDA) proudly debuted its Downtown Berkley Shopping Bag for a Cause through a partnership between Better Life Bags.

Supporting new and existing small businesses, and the entrepreneurs who run them, represents a vital aspect of the revitalization of downtowns and neighborhood business districts.

The Equitable Economic Development Fellowship is a two-year, one million-dollar effort funded by the Surdna Foundation and the Open Society Foundations to help equity, transparency, sustainability and community engagement become driving forces in local economic development efforts.

The Jefferson Rotary Club partnered with Jefferson Matters: Main Street to offer mini-grants for building facades and storefront signage to two dozen businesses for up to $500 each.

The Wisconsin Economic Development Corporation (WEDC) partnered with Retailworks, Inc., a commercial interior design, display and branding firm headquartered in Milwaukee, to launch Wisconsin’s Main Street Makeover Contest.

Too often, as we’re strolling our favorite Main Street, we pass empty or dark shop windows that make us want to hurry home a little bit faster. Imagine instead, a charming streetscape adorned with vibrant, lively window displays, showcasing retailers’ favorite products and seasonal gift ideas.

Small Business Saturday promo pic from Downtown Goldsboro, North Carolina, showing all the folks who took the pledge support a small business in their community.

We’ve put together a practical list of some of the things that local store owners can do right now to help them capitalize on this increasing trend in local searches.

From authentic comfort food to farm-to-fork fresh and everything in between, these restaurants, bars, and cafes are key to the thriving social, business, and residential life in the historic commercial districts in Main Street Iowa communities.

Located in southeast Kansas, Independence (pop.8,799) is home to Fab Lab ICC, which is on track to be the world’s leading innovator in combining entrepreneurial mindset education with a fab lab maker space.

Being the only person in the know can be fun, exhilarating even. Except when you are the one person out of 600+ in a room and you know bad news is coming.

Fritz the dog has made his way into the hearts of the residents of LaBelle, Florida, and helped our Main Street Community find a way to make what we do more noticeable.

Altavista On Track, the local Main Street organization, is working to cultivate and sustain local entrepreneurs with an educational business launch competition, Pop-Up Altavista 2.0.

The first rule of conducting business is “make it simple.” The easier it is to pay for merchandise, get entertainment or obtain a service, the more likely it is that people will take advantage of those options.

Main Street communities across the country are no stranger to seeking creative strategies to solve their most nagging issues – vacant buildings, marketing downtown, bolstering retail to name a few.

To understand the role that immigrant business owners play in Boston’s small business ecosystem, you need only to walk through any Boston Main Streets district.

A lot of signs are necessary to make a downtown work well, but not every community knows what a good sign system looks like, or how instrumental it can be to the creation of a successful downtown.

Main Street Iowa, a program of the Iowa Economic Development Authority’s Iowa Downtown Resource Center, created a one-of-a-kind three-year program to provide help for performance venues located in Main Street districts.