May 22, 2019 | Main Spotlight: What’s In Your Backpack? South Carolina Releases Economic Incentives Toolkit | By Jenny Boulware, Main Street South Carolina |

The Western Auto building (1940) and the Rose-Talbert building (1914) were renovated together in 2018. Hotel Trundle was designed by BOUDREAUX, in association with POND interiors. The Hotel occupies both floors and features 41 rooms. Before photo by Roger Lewis. After photo by BOUDREAUX

The Western Auto building (1940) and the Rose-Talbert building (1914) were renovated together in 2018. Hotel Trundle was designed by BOUDREAUX, in association with POND interiors. The Hotel occupies both floors and features 41 rooms. Before photo by Roger Lewis. After photo by BOUDREAUX

One of the primary goals of all Main Street Programs is to increase the value of downtown by improving its commercial environment while encouraging historic preservation. Improving the local commercial economy is often one of the most difficult challenges confronting a Main Street program. However, numerous national, state and local incentives already in existence can boost downtown redevelopment efforts.

In fact, South Carolina has one of the best tax incentive packages in the United States. These incentives can add up to savings in some cases as much as 25%, 50% or more of the cost of rehabilitation. Many of these incentives are overlooked by landlords, businesses and the development community. To shine a light on these substantial cost savings, Main Street South Carolina created an incentives toolkit to encourage downtown development and reinvestment. The incentives featured include:

- Federal Historic Rehabilitation Tax Credit

- SC State Historic Tax Credit

- Federal New Markets Tax Credit

- SC State Abandoned Building Credit

- Bailey Bill Property Tax Incentive

Learn more about the process and uses of the toolkit here for inspiration on how to create a toolkit of your own and check out a summary of the incentives and projects featured below. A downloadable PDF version of the toolkit will be available in the near future.

Federal Historic Rehabilitation Tax Credit

-

Available for costs incurred when rehabilitating historic buildings for income-producing uses.

-

The credit is equal to 20% of Qualified Rehabilitation Expenses, and can be used to offset a corporate investor’s federal income tax liability.

-

QREs do not include acquisition costs for land and building.

-

The corporate investor “purchases” credits by buying an equity interest in the entity that owns the building. Credits are generally allocated to the owners in accordance with their allocation of profits. However, cash flows are allocated differently than profits through the use of various fees and other structuring methods.

Requirements

- Property is listed on National Register of Historic Places.

- Property is not tax-exempt.

- Taxpayer completes a Historic Tax Credit Application.

- QREs undertaken during a 24-month measurement period.

- Project is not an enlargement of current structure.

- Development fees must be “reasonable.”

Benefits

- 20% income tax credit is based on QREs undertaken in the measurement period.

- 100% becomes available the year property is placed in service.

- Can be carried back one year and carried forward for 20 years.

- A five-year recapture period applies for the credits, in which the investor must keep its interest in the project. After the recapture period expires, the developer or general partner usually has the option to purchase the investor’s interest for a fraction of the investor’s initial investment.

PROJECT EXAMPLE

Curtiss-Wright Hangar | Columbia, SC

The building was built in 1929 and added to the National Register of Historic Places in 1998. It was renovated in 2017 as an adaptive reuse for a craft brewery. Before and after photos by Roger Lewis

The building was built in 1929 and added to the National Register of Historic Places in 1998. It was renovated in 2017 as an adaptive reuse for a craft brewery. Before and after photos by Roger Lewis

SC State Historic Tax Credit

- Piggybacks on the Federal Historic Tax Credit for purposes of qualifying projects, defining Qualified Rehabilitation Expenses, calculating credit amount.

- The credit can be used to offset any SC tax imposed under Title 12 of the SC Code of Law. Generally, it is used to offset the state corporate income tax.

- Credit must be used to equal installments over a three-year period. Any unused portion may be carried forward for a five-year period.

Requirements

- Taxpayer applies using the federal application for the Historic Tax Credit.

- Minimum investment for owner-occupied residential is $15,000 and is limited to one structure every 10 years.

Benefits

- Credit is equal to 10% of QREs or an election can be made to take a credit based upon 25% of QREs. If the developer chooses the 25% option, the credits are limited to $1 million.

- Credit is applicable against state income and insurance premium taxes.

- May offset 100% of taxpayer’s liability.

- Extra credits carry forward for five years.

- One-year credits taxed as transferrable credits.

PROJECT EXAMPLE

BOUDREAUX Offices | Columbia, SC

Built in 1920, the Powell Furniture building is included in the Columbia Commercial Historic District. It was renovated in 2018 to house Hotel Trundle on the first floor and BOUDREAUX offices on the second floor. Design and photos by BOUDREAUX.

Built in 1920, the Powell Furniture building is included in the Columbia Commercial Historic District. It was renovated in 2018 to house Hotel Trundle on the first floor and BOUDREAUX offices on the second floor. Design and photos by BOUDREAUX.

Federal New Markets Tax Credit

- Available to investors in Community Development Entities for qualifying investment the CDEs make in those businesses that are located in low-income communities.

- The best way to utilize this credit is to find an existing CDE that already has an allocation and convince them to loan the developer funds for a project, likely at a low interest rate.

Requirements

- Commercial real estate qualifies as a business for the purposes of CDE investments.

- Investment by the CDE can be in the form of a loan or equity.

- The CDE must receive allocation from the federal government for the credits.

- The CDE can provide the owner/developer an interest-only loan for 20% of the project cost which loan is “forgiven” after five years.

Benefits

- Credit is equal to 49% of the amount of the CDE’s investment.

- 5% for each of the first three years.

- 6% for years four to seven.

PROJECT EXAMPLE

Claussen Bakery | Greenville, SC Built in 1930, Claussen Bakery was a former family-owned bakery in the West End of Greenville. In 2009, a real estate partnership acquired the property. In 2014 they began renovating the building and surrounding land to accommodate office and other commercial business. McMillan, Pazdan, Smith Architecture serves as the anchor tenant, occupying the 2nd floor, while 16,500 square feet of 1st floor commercial space is available to small businesses.

Built in 1930, Claussen Bakery was a former family-owned bakery in the West End of Greenville. In 2009, a real estate partnership acquired the property. In 2014 they began renovating the building and surrounding land to accommodate office and other commercial business. McMillan, Pazdan, Smith Architecture serves as the anchor tenant, occupying the 2nd floor, while 16,500 square feet of 1st floor commercial space is available to small businesses.

SC State Abandoned Building Credit

- ABC is available for rehabilitation of abandoned buildings and the surrounding site.

- Incentive provides either an income tax credit or property tax credit for the renovation, redevelopment or improvement of abandoned building sites operated for income-producing purposes.

- Legislative repeal of ABC is expected to become effective on December 31, 2021.

Requirements

- Taxpayer must send a Notice of Intent to Rehabilitate the site to the municipality (or county of an unincorporated area) where the site is located.

- Site must be at least 66% abandoned (the space has been closed continuously to business or otherwise nonoperational for income-producing purposes) for the five-years preceding the Taxpayer’s Rehab Notice.

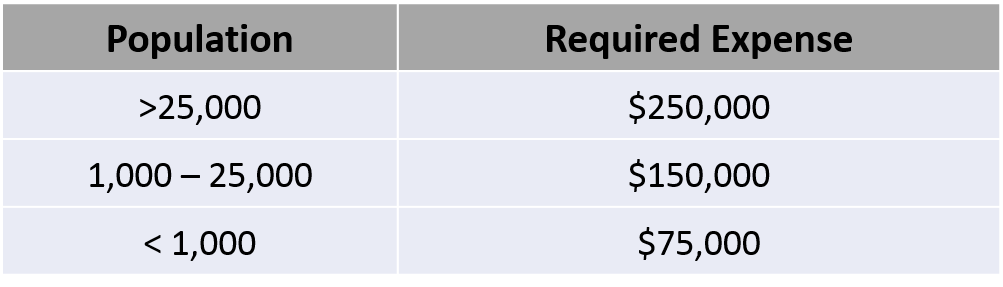

- Taxpayer must incur certain required expenses at the site, as determined by the population of the municipality or unincorporated area.

- Taxpayer may apply to the governing body for certification that the site is abandoned.

Benefits

- ABC is equal to 25% of expenses incurred at the site, taken in equal installments over a three-year period (maximum of $500,000 per site).

- The ABC can either act as:

- A credit against taxpayer’s income taxes or corporate license fees, or

- A credit against real property taxes at the site (equal to 75% of the Site’s real property taxes for up to eight years, by ordinance).

- ABC amount is based on actual or estimated expenses as follows:

PROJECT EXAMPLE

McCants School | Columbia, SC

Built in 1931, Fannie McCants Elementary School was named for Columbia High School’s first full-time librarian. It is adaptively reused as townhomes in Earlwood Park. Before and after photo by Rogers Lewis

Built in 1931, Fannie McCants Elementary School was named for Columbia High School’s first full-time librarian. It is adaptively reused as townhomes in Earlwood Park. Before and after photo by Rogers Lewis

Bailey Bill Property Tax Incentive

The governing body of a county or municipality may grant by ordinance certain special property tax assessments to real property qualifying as “rehabilitated historic property” or as “low and moderate income rental property.”

Requirements

- Upon preliminary certification by the taxing entity, the owner-occupied property is assessed for two years based on a special valuation equal to the fair market value of the property at the time.

- Property is eligible for preliminary certification if:

- Owner applies for and is granted a historic designation by the taxing entity; and

- The proposed rehabilitation receives approval by the appropriate reviewing authority.

- Depending on the property’s location, the appropriate reviewing authority could be:

- The county board of architectural review;

- Another qualified entity with historic preservation expertise; or

- The South Carolina Department of Archives and History.

- Upon completion of the project, the property must receive final certification from the taxing-Entity to obtain its final special valuation.

- Property is eligible for final certification if:

- It has received its historic designation;

- The completed rehabilitation has been approved by the appropriate authority; and

- The project has incurred the “minimum expenditures for rehabilitation” established by ordinance.

- To be qualified as low-moderate income rental property, the property must also meet requirements of SC Code Section 4-9-195(C) in order to receive the final certification.

- Upon the final certification, the property’s final valuation will equal to its fair market value at the time of preliminary certification (or equal to the fair market value at the time of final certification, if no preliminary certification was obtained).

Benefits

- The property is assessed at its final valuation for the lesser of either 20 years, the period established by ordinance, or the year of the property’s disqualification.

- Disqualifying events are given in South Carolina Code Section 4-9-195(E).

PROJECT EXAMPLE

First National Bank of Clinton | Clinton, SC

Converted into a mixed-use space with three market-rate apartments upstairs and three commercial spaces on the ground floor. Before photo by City of Clinton. After photo by City of Clinton

About the author:

Jenny Boulware is the Main Street South Carolina Coordinator at the Municipal Association of South Carolina. Main Street SC is the nation’s only program housed within a municipal league. Boulware provides technical support and leadership for the implementation of the Main Street Approach in 26 Main Street programs across South Carolina. With 20 years of experience in downtown revitalization, community development and economic development she is thrilled to direct South Carolina’s program. jboulware@masc.sc, 803.354.4792