Announcing the Science Discovery on Main Street Grant Recipients

Main Street America is thrilled to announce the 12 Science Discovery on Main Street grant program recipients.

Ellicott City Flood Recovery | The historic structures requiring stabilization -- they are missing the supporting wall and load bearing columns.

Credit: Preservation Maryland / Flickr CC BY-NC-SA 2.0

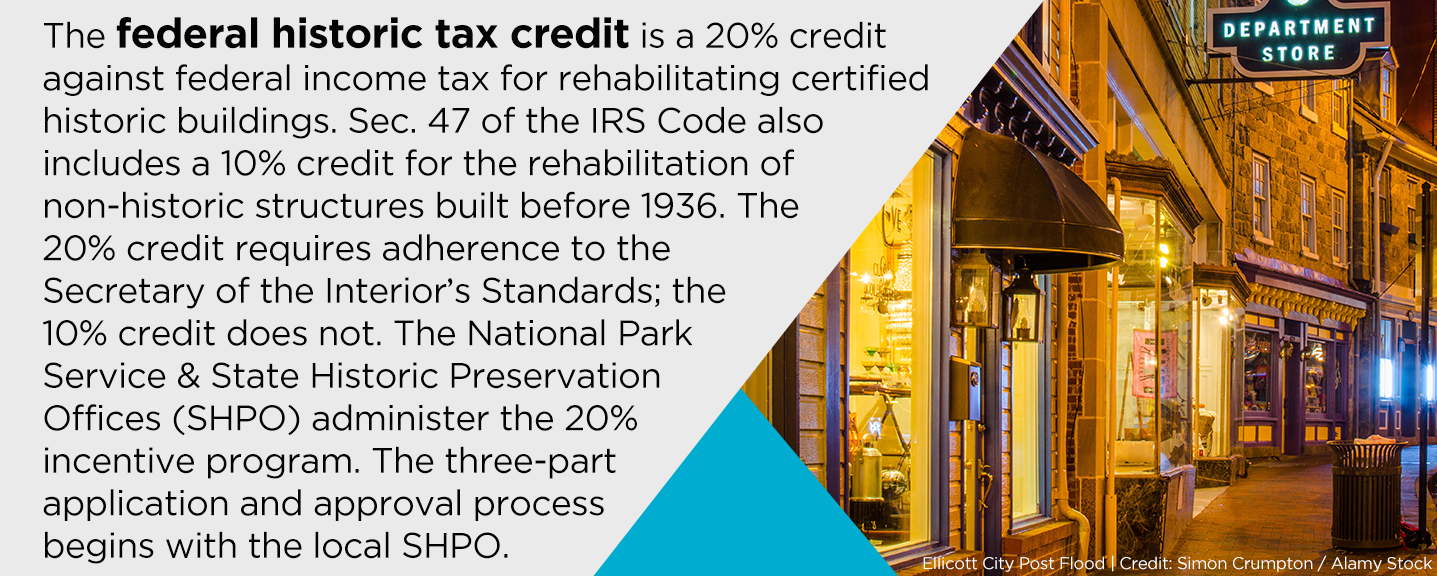

Both Houses of Congress have promised to produce draft legislation to overhaul the federal tax code in September 2017. On the table for possible elimination is the federal historic tax credit (HTC). As one strategy to meet this threat, legislators in both houses have introduced legislation, the Historic Tax Credit Improvement Act (HTCIA), which would modernize the HTC in the context of a reformed tax code. As described in the following article, the HTCIA would address many of the barriers to the use of the HTC for small Main Street transactions. Main Street organizations are urged to contact their Congressional delegations to co-sponsor this bill and protect the HTC from elimination under tax reform. Consider signing the National Trust’s advocacy letter and hosting a site visit for your Members of Congress during the August recess. For help, contact Shaw Sprague at ssprague@savingplaces.org

On July 30, 2016, after six inches of torrential rain, a flash flood roared down Main Street in Ellicott City, Maryland, a vibrant 18th century commercial district. Located at the confluence of Tiber Creek and the Patapsco River, this popular destination for Baltimore and Washington residents has been plagued many times over the years with damaging floods. This time, tragically, two people died, hundreds of cars were damaged or destroyed and scores of businesses were shuttered. Just under one year later, in a remarkable turnaround, 90 percent of the commercial properties are now back in service. Ellicott City is a certified Main Street Maryland community.

In the midst of this human and cultural disaster, the Main Street program, managed by the Ellicott City Partnership, collaborated with Preservation Maryland to provide a variety of disaster relief financing that helped expedite the recovery. Preservation Maryland set up a field office to provide technical assistance to property owners who qualified for the federal and state historic tax credits (HTC). The Main Street program focused on short-term emergency grants to defray the costs of immediate health, transportation and safety concerns. Main Street’s programs, described in more detail below, were a hit. But in the end, only a few buildings utilized the federal credits to help finance damage repair. (See below for a refresher on 20 percent and 10 percent HTC basics.)

What went wrong? And what does it tell us about the federal HTC and its accessibility to Main Street property owners and merchants? What improvements to this nearly 40-year-old tax incentive would increase its usage on Main Street? This article attempts to answer these questions through an analysis of what financing options were pursued by Ellicott City Main Street property owners and why.

For this article, several role players in this disaster and recovery story were interviewed including the Maryland Historical Trust (SHPO), Preservation Maryland’s field office manager, the Howard County Department of Planning and Zoning, the Main Street program and several property owners.

Disaster Relief Options Available to Property Owners

Renee Novak, an architectural historian, was selected by Preservation Maryland to manage its disaster assistance field office. She conducted workshops, offered individual consultations and filled out HTC applications. She described “layers” of other financing options through Main Street, and county, state and federal government programs. Renee said that while these various sources of relief were utilized, many property owners complained of “application fatigue.”

The State Historic Preservation Office (SHPO) reported that among scores of property owners, only four applied for federal tax credit support only. Significantly, three of those applications were for certification of non-contributing building status, an indication that the owners hoped to utilize the federal 10 percent non-historic building credit. This credit does not require SHPO and NPS design review and has no application and approval process. Owners often utilize the 10 percent credit to avoid the design requirements and added costs of complying with the Secretary’s Standards. Of the two applications for combined federal and state HTCs, one building has received Part 3 certification and another is at the Part 2 stage. Doug Harbit, Development Director at Preservation Maryland, said his organization was “astonished” at how few owners applied. The state’s low-interest loans were much more popular. Twenty-two owners received state loans and twelve closed on SBA loans.

Ellicott City Recovery Press Conference, Nick Redding | Preservation Maryland Executive Director Nick Redding speaking at a press conference on the restoration and rehabilitation of Old Ellicott City. Howard County Executive Allan H. Kittleman stands behind him.

Credit: Preservation Maryland / Flickr CC BY-NC-SA 2.0

The Main Street program, in partnership with United Way, raised over $1.8 million in donations, and operated five separate relief programs that helped 190 residents, 90 businesses and 81 property owners. In the immediate aftermath of the flood, $95,000 was distributed to upper floor residents and business and property owners in the form of $500 Ellicott City Strong mini-grants and gift cards. Another $80,000 was provided through a Safe Cleanup grant program to hire professionals to clean up properties deemed an immediate health hazard. In collaboration with Heritage Automotive, $50,000 in matching automotive grants were provided to residents, businesses and properties owners whose cars were destroyed to help them buy new cars. Preservation Maryland is also in the process of awarding grants from a $50,000 disaster fund. Owners report that they could not purchase flood insurance because their businesses were located in a flood plain. Nor were FEMA grants available since commercial businesses are not eligible.

Howard County offers a property tax credit for up to 25 percent of eligible rehabilitation expenses. It also set up a special façade improvement grant program. To cut red tape for the grants and credits, the county required that its Historic Preservation Commission meet bi-weekly instead of monthly. They also coordinated inspections and permitting from the other county departments including health and building codes.

Through many workshops and technical services, Ellicott City property owners were well-informed of their disaster relief options. With so many applications to fill out, owners clearly preferred some programs over others. The stats indicate that the county’s offerings, Main Street grants and state low interest loans were much more popular that the federal and state HTCs; this despite the fact that Preservation Maryland’s field office literally drafted tax credit applications ready for signature. Most were never sent in.

Ellicott City Flood Recovery | Mat Daw of Keast & Hood Structural Engineers meets with representatives of the Structural Group to plan the stabilization of these structures.

Credit: Preservation Maryland / Flickr CC BY-NC-SA 2.0

Case Study

Michel and Angie Tersiguel of Tersiguel’s French Country Restaurant, provided an interesting case study of how they financed approximately $250,000 in repairs. Damage was greatest in the basement and first floor of their 19th century building including the loss of two walk in freezers and the entire wine collection. As flood waters reached the first floor, staff had to relocate diners to the second floor for safety.

Taking advantage of help from Preservation Maryland, Michel and Angie applied for and received state and federal credits with a combined value of approximately $75,000. They also received a $50,000 low-interest loan from the state and $40,000 from a crowd sourcing campaign set up by friends. The balance of the costs were funded out of pocket. The Tersiguels could not obtain flood insurance and receive nothing from their property insurer.

Michel and Angie were generally grateful for the federal and state HTC assistance. However, Michel did say the programs required a high learning curve and could not provide the kind of immediate funding he needed to reopen in October of 2016. Because he and his wife could not access outside investors to provide immediate cash for the relatively small amount of credits they earned, Michel and Angie will keep the credits for their own use. But their limited annual federal tax liability will require that they carry the credits forward many years to eventually reimburse themselves for some of their repair costs. This forced the couple to “bridge” the receipt of the tax credits by putting money out of pocket to pay contractors to complete the work.

What Factors Influenced Property Owners Decision on Whether to Use the HTCs?

Preservation Maryland’s experience marketing the federal and state HTCs and feedback from owners have revealed an interesting mix of factors that ultimately led to a low utilization of federal and state HTCs compared to other disaster repair financing options.

Timeliness – As indicated by the experience of the Michel and Angie Tursiguel, the ability to turn credits into cash in time to pay the contractors is very difficult on small transactions for which there is no investor market. Owners who do not have the liquidity, cannot afford to wait many years to recoup the value of the credits. Timeliness of the application process was also a factor. At a point when owners were desperate to put their buildings back in service as soon as possible, the two-step state and federal HTC process proved too long to help with the immediate crisis despite efforts by the SHPO and National Park Service to be responsive to the crisis.

Lack of Owner Access to Investor Capital – This age-old issue for the tax credit industry put HTC usage at a disadvantage to various public and private grant funding and property tax credits. According to Renee Novak, owners were primarily interested in cash “now”, not later. The earliest tax credit proceeds to an owner who uses the credits to defray his/her own federal tax liability is not until tax returns are received the year after the building is placed back in service. Outside investors generally contribute most of their tax credit equity to the partnership before construction completion.

The Secretary’s Standards – It was revealing that three of the four federal applications reported by the state were to obtain non-conforming building status so that the owners could use the 10 percent credit which avoids the need to meet the Secretary’s Standards. Some owners noted that the Standards substantially increased the cost of repairs.

The Substantial Rehab Test - Under current HTC law, an owner must spend at least his/her “adjusted property basis” or $5,000 whichever is greater to qualify for the federal HTC. Adjusted basis is what you paid for the property, plus the cost of any prior improvements, less the value of the land and any depreciation already taken by the owner. Some potential applicants noted that the substantial rehab test would force them to spend more than they needed to place their buildings back in service.

Preference for Dealing with Local County Officials and Programs – Renee Novak reported that owners preferred dealing with nearby county officials and review boards. With limited travel schedules, SHPOs and National Park Service reviewers do fewer site visits than they would like. Howard County officials were minutes away and, as noted earlier, expedited their services to meet the needs of the property owners.

How could the Historic Tax Credit Improvement Act Help Main Street Access the HTC?

The Ellicott City story provides insight into what changes to the federal HTC might have helped a greater number of property owners. Current legislation with broad Senate and House support, the Historic Tax Credit Improvement Act or HTCIA (HR 1158 and S 425), would make several overdue changes to the federal HTC that would address many of the barriers Main Street property owners like those in Ellicott City face when considering the use of the federal HTC. Achieving a better balance between urban and small town locations and large and small transactions are the heart of the HTCIA legislation. Key provisions include:

While the 30 percent credit gets a lot of attention, the ability to sell a tax certificate instead of forming a complicated partnership with an outside investor would address the lack of investor interest in small deals. Bill sponsors believe that a new market of small deal investors, typically individuals, would likely develop for the federal HTC similar to what we have seen in 19 states that allow state HTC transfer via tax certificate.

The third provision addresses the perverse incentive under current law to spend more money on improvements than the building needs. SHPOs have reported that in rural towns, appraisals typically do not support this level of spending. Most states have already departed from federal law by lowering their minimum rehabilitation requirements to amounts such as $50,000.

The current interest in federal tax reform is the worst threat the HTC has faced since the code was last reformed in 1986. It is also the best opportunity the preservation community has had to make long overdue changes that would make the federal credit more accessible to Main Street.

Here’s How You Can Help

Sign your organization onto national letter.

Request a meeting with your members of Congress during August recess.

Send your members of Congress a request to co-sponsor the Historic Tax Credit Improvement Act

ABOUT THE AUTHOR:

John Leith-Tetrault supports the National Trust Community Investment Corporation (NTCIC) public policy efforts by engaging in high-level policy discussions with federal lawmakers and executive branch officials on a number of important issues, including comprehensive tax reform, historic tax credit (HTC) eligibility for the Community Reinvestment Act (CRA), legislation to modernize the HTC, IRS tax treatment of HTC transactions and improvements to the National Park Service’s administration of the HTC program. John chairs the Historic Tax Credit Coalition (HTCC) which has led the effort to retain the HTC in a reformed tax code. The HTCC also worked closely with the IRS to develop Revenue Procedure 2014-12 that governs how HTC transactions are structured to comply with the Historic Board Walk Hall appeals court decision. John has a Masters Degree in Urban Planning from George Washington University and a BA in History from Georgetown University. He brings over 40 years of real estate, community development, banking and tax credit experience to NTCIC. In addition to his 15 years as the founding President of NTCIC, John’s experience includes employment in various community development financing capacities with the following organizations: Neighborhood Housing Services, NeighborWorks USA, Enterprise Community Partners, Bank of America and the National Trust for Historic Preservation.

Main Street America is thrilled to announce the 12 Science Discovery on Main Street grant program recipients.

Learn how to leverage the Main Street Approach during natural disaster recovery.

Creating real change in business ownership starts with local communities leading the way, backed by strong partnerships and collaborations.

Learn how Main Street America's work with the DOT's Thriving Communities Program is supporting transformative efforts with community partners like the Shoalwater Bay Indian Tribe.

Becky Axilbund, Executive Director at Main Street Middletown, MD Inc., shares lessons learned from their renovation of two downtown buildings.

For Preservation Month, Senior Program Officer Lisa Mullins Thompson explores why preservation matters and how Main Streets can celebrate and protect their historic assets.

Nevada, Iowa © Main Street America

At Fort Vancouver in Vancouver, Washington, Native Hawaiians played a critical role in the success of the Hudson Bay Company. Today, Vancouver’s Hawaiian history and heritage plays a crucial role in efforts to reenergize the city’s historic downtown.

Understanding the Advisory Council on Historic Preservations report on federal historic preservation standards.

Toccoa, GA © Steph Maley

In this video, learn more about the Williams’ family story, how the business is helping to revive downtown Helena, and the impact they’re having on a national level.

Learn how Albany, Georgia, recognizes their civil rights legacy and supports the African American community today.

Kathy LaPlante shares her experiences visiting Vermont communities during their recovery from devastating floods.

© Tripp Muldrow

In honor of National Disaster Preparedness Month, we are providing some practical steps that Main Streets can take to prepare for the next, inevitable disaster.

© Adog

Learn the historic and cultural significance of neon signs, and strategies that Main Streets can use to preserve these unique assets.

Main Street America is leading a coalition urging that the EPA make available the GGRF funds for adaptive reuse and location-efficient projects because of the substantial greenhouse gas emissions reduction offered by such developments.

On May 9, the National Trust for Historic Preservation released its list of America’s 11 Most Endangered Historic Places for 2023 which included a cultural district located within a designated Main Street America community.

Miami, FL © NTHP

From 19th-century mill girls to Maine's mill redevelopments and the regional manufacturers of tomorrow, learn about the amazing history and promise of the New England mill.

Biddeford, ME © Heart of Biddeford

Learn the unique history of Folsom, New Mexico, and how they are working with New Mexico MainStreet today.

This article was published on January 10, 2023, by Next City, a nonprofit news organization focused on socially, economically, and environmentally sustainable urban practices.

Learn how Rethos, the Coordinating partner for Minnesota Main Streets, has partnered with Reuse Minnesota and the Minnesota GreenCorps Program to encourage community-led preservation.

© Rethos

Four recommendations that Main Street districts can apply right now to start preparing for the next natural disaster.

Learn how Main Streets can partner with the National Trust Community Investment Corporation to take advantage of the Historic Tax Credit.

© Troy Thies

Ed McMahon shares recommendations and insights on how Main Streets can use sign design to improve sense of place on Main Streets.

Main Street organizations and other public-private partnerships can provide the focal point needed to fulfill the large number of roles required to reuse or redevelop a house of worship in a way that benefits the community.

Learn about The Bottom, a historic African-American community in Thomasville, Georgia, and efforts to preserve it's history and share it's story.

Thomasville, GA © City of Thomasville

New Mexico MainStreet partnered with Main Street America to utilize a NPS Main Street Facade Improvement Grant.

Gallup, NM © New Mexico MainStreet

How do those amazing Main Street rehabilitation projects happen? And what policies and public support make them happen? In the Behind the Ribbon Cutting series, we look at a project or businesses from concept to opening day to break down the partnerships and funding brought to bear and recognize how we can advocate for policies and resources for revitalization across the country.

Astoria, OR © ADHDA

Main Street America's GIS intern shares the results of a project to map the boundaries of all designated Main Street districts.

Main Street America welcomed the National Association For Latino Community Asset Builders (NALCAB) to our Twitter channel to share stories of resiliency in Latino communities.

Main Street America welcomed to our Instagram Stories the Allapattah Collaborative CDC, a Main Street program in Miami, Florida.

Miami, FL © Allapattah Collaborative CDC

We sat down with Lindsey Wallace, Director of Strategic Projects and Design Services and manager of the the National Park Service Main Street Community Disaster Preparedness and Resilience Program, to learn more about her perspective on disaster preparedness on Main Street.

To support Georgia Main Streets throughout the recovery process and position them for long-term sustainability, Main Street America launched the Georgia Main Street Innovation Grant Program, made possible through generous support from The Williams Family Foundation of Georgia.

Thomasville, GA © Thomasville Main Street

The Association for Preservation Technology International (APT) Main Street Task Force is working to increase education, compile examples and data, and provide recommended changes at the national level where necessary.

From community gathering spaces to retail incubators, from small towns to big cities – this year’s projects and communities are a testament to the diversity of Main Streets across the country.

The Main Street America Institute (MSAI) partnered with the National Development Council (NDC) to offer Historic Real Estate Finance, part one of a two-course certificate program, in Des Moines, Iowa.

Texas First Lady Cecilia Abbott joined Texas Main Street and Texas Historical Commission staff, management and Commissioners to welcome Temple and Pearsall into the 89-city Texas Main Street network.

As part of the Community Foundation of Greater Atlanta’s Grants to Green program, Maine was designated one of two national replication sites.

After more than five years of consistent advocacy, the 20 percent historic tax credit (HTC) has survived the most significant rewrite of the tax code in more than 30 years.

In the wake of Hurricane Harvey, Main Street merchants in two communities in Michigan and Kentucky, as well as a fellow Texas Main Street community, jumped in to help their Texas colleagues.

In 2016, the North Carolina Main Street & Rural Planning Center partnered with the University of North Carolina at Greensboro’s Department of Interior Architecture (UNCG) to provide design assistance to Main Street communities.

In 2015, the Wisconsin Economic Development Corporation (WEDC) partnered with the University of Wisconsin–Madison to engage Wisconsin Main Street organizations and farmers markets in the Metrics and Indicators for Impact – Farmers Markets (MIFI-FM) toolkit.

With 413 National Park areas¹ and over 1,000 Main Street America programs, it’s no surprise that many of the communities following the Four Point Approach serve as gateways to our national parks.

Eight historic downtowns in Vermont turned massive flooding into opportunities to build back stronger than before the flood.

As living pieces of American history, our Main Street communities each have a story to tell. It’s up to us to bring those stories to life.

The economic value of historic preservation on Main Street.

We measure the effectiveness of our last marketing campaign, weigh whether the investment in new street lights outweigh the political capital spent, and debate if the thousands of volunteer hours are worth the impacts created by a one-day event.

Main Street Iowa, a program of the Iowa Economic Development Authority’s Iowa Downtown Resource Center, created a one-of-a-kind three-year program to provide help for performance venues located in Main Street districts.